Chapter 1 - Crisis to Growth:

Strategies for Recovery in the Asia-Pacific

The recovery of the Asia-Pacific from the global economic crisis of 2008-09 is underway, but the region still faces considerable unemployment and the twin challenges of exiting interventions adopted in the crisis and implementing new structural policies to drive growth. This will be a difficult transition and there is still ample risk of slow growth and persistent unemployment, reemerging global imbalances, and financial volatility.

This chapter is based on the report of a task force commissioned by the Pacific Economic Cooperation Council (PECC) in March 2009 to see what the Asia-Pacific should do in response to the global economic crisis.*

Chart 1-1: Real GDP Growth Projections (IMF, October 2009)

* The members of the task force members are: Yongfu Cao, Chinese Academy of Social Sciences, Wendy Dobson, University of Toronto, Yiping Huang, Peking University, Peter A. Petri (coordinator) Brandeis University & East West Center, Michael Plummer, Johns Hopkins University & East West Center, Raimundo Soto, Catholic University of Chile, and Shinji Takagi, Osaka University. The taskforce would like to also acknowledge the valuable feedback from an international panel of advisors. The report of the taskforce will be published in 2010.

The policies that stopped the economic freefall – huge stimulus packages in China, the United States and even small economies like Singapore, and massive financial bailouts in the West – were urgent, relatively easy to sell politically, and to a large extent forced by circumstances (particularly the fall of Lehman Brothers). They were deployed under extraordinary time pressures and have proved remarkably successful.

But sustained recovery will require tackling different problems, including international imbalances between the United States, China, and other economies. U.S. consumers are not likely to drive world demand in the medium term, and the slack will have to be taken up in part by Asian consumption and investment. The early responses to the crisis were not designed to address these issues, and some are even counterproductive from that perspective.

The best outcomes – inclusive, balanced, sustained growth – will require structural reforms that change economic relationships within economies and among them. The policies required to achieve such a path are complicated and varied, addressing household and government finances, investment incentives, risk management, infrastructure, productivity, social and environmental priorities, and other fundamental aspects of growth.

Crisis, recovery and risks

The crisis originated, as is now well known, in the highly leveraged financial sector of the United States. It simmered from early 2007 until the collapse of Lehman Brothers in September 2008, and then spread swiftly through the Asia-Pacific and the world. Because Asian financial systems survived the early phases of the crisis relatively well, some observers had hoped that the region was “decoupled” from North American business cycles. But the crisis did hit Asia, and very forcefully so through the trade channel. Most Asia-Pacific economies experienced sharp declines in exports, output and employment, and plummeting asset prices. A few – China, Indonesia – continued to grow even at the bottom of the crisis, but others, notably Asian exporters of advanced manufactured products, became its most severely affected casualties.

Asia-Pacific governments led the world in the speed and scale of policy responses. Monetary and financial measures included sharp reductions in policy interest rates in nearly all economies. Central banks intervened deeply in a wide range of markets; for example, the Federal Reserve System of the United States more than doubled its balance sheet in just two months in the fall of 2008. Large fiscal measures followed. Together, Asia-Pacific economies adopted stimulus packages of $1.7 trillion, or 84% of the estimated total world-wide discretionary stimulus, 1 including $0.6 trillion in China and $0.8 trillion in the United States. Singapore, Mexico and many other economies also responded with major stimulus efforts.

Chart 1-2: Fiscal and Monetary Measures

1 European economies had somewhat stronger automatic stabilizers operating through the crisis.

Given the severity of the global shock, the first “green shoots” of recovery appeared surprising quickly. In 2009 Q2, the Chinese economy began to accelerate, and Japan, Korea, Singapore and other economies that were especially hard hit in previous quarters returned to growth. By the 2009 Q3, the United States had also turned the corner. The reasons for these early successes were large stimulus programs, recovery from negative stock-adjustments early in crisis, and the basic resilience of Asia-Pacific economies. In mid-2009, forecasters began to revise projections upward and converged toward describing the crisis as a deep “V” and some economies such as Australia have begun to raise policy interest rates.

Yet in late 2009 a full recovery is far from assured. Adverse outcomes are especially likely if China and/or the United States are unable to transition to balanced growth. In the US, this might be due to continued weakness in the financial sector and large government deficits; in China, it might be caused by excessive bank lending for investment. Poor outcomes could also follow from premature tightening of monetary or fiscal policies; insufficient demand due to entrenched unemployment and other structural problems; persistent financial fragility due to the drag of bad assets on the financial sector; and expanding international imbalances that trigger asset price and/or currency volatility. Since governments have exhausted many policy options in recent months, they have little ammunition left to fight another setback, should one occur.

Sustained growth beyond the crisis

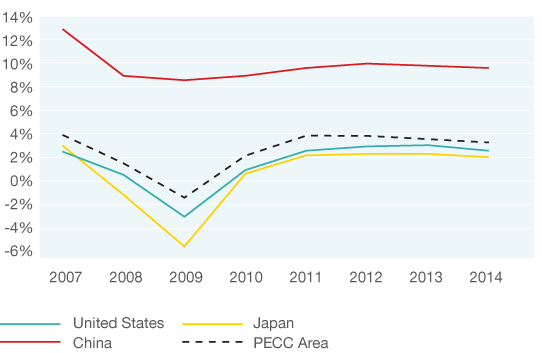

The term “rebalancing” is widely but imprecisely applied to policies that address some of these threats, and especially global imbalances. Before the crisis, unsustainable borrowing supported high US consumption, while unprecedented savings – including more than half of China’s national income – went into unsustainable investments in export industries and dollar assets. These internal imbalances in expenditures led to large international imbalances in terms of trade and capital flows between the United States and China, Japan and other economies.

Harsh market adjustments have reduced these imbalances during the crisis. The US current account deficit declined to under 3 percent of GDP, a level widely considered sustainable. U.S. consumers are attempting to rebuild savings, and imports by US and European consumers are likely to stay sluggish for some time. To compensate for these trends and to orient Asia-Pacific production toward expenditures that are sustainable in the medium term, producers across the region will need to depend increasingly on Asian consumption and investment demand, rather than net exports.

Some current forecasts – including by the IMF – foresee US external deficits remaining at sustainable levels, but not all are optimistic. For example, William Cline (2009) projects lower world growth rates and higher imbalances; in one simulation he sees US current account deficits rising to 5.2 percent of GDP by 2011 and eventually to 16 percent of GDP by 2030. This scenario is based on the assumption that the US will not reduce its government deficits and that foreign investors (especially China) will continue to buy US assets despite growing debt. This would be a risky path. Once markets recognize that imbalances are not under control, currency and asset markets would likely become volatile, perhaps triggering another downturn.

Avoiding large new imbalances is thus an important prerequisite for a sustained recovery. We find, however, that the arithmetic of this challenge is manageable. Even at its maximum before 2007, the “excessive” part of the U.S. deficit (the portion above 3 percent of GDP) amounted to little more than $300 billion. This is a large value, but one that needs to be viewed in the context of the Asia- Pacific region’s $28.8 trillion economy.

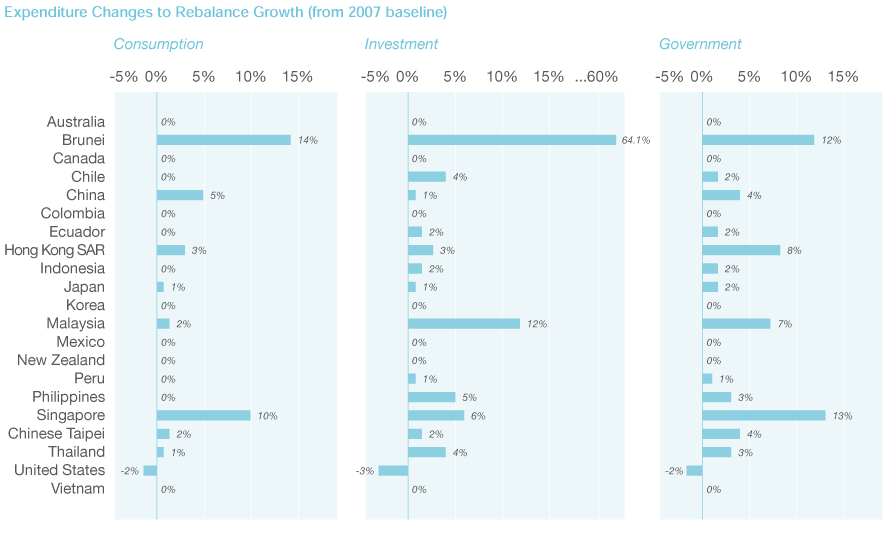

Chart 1-3: Rebalancing Demand

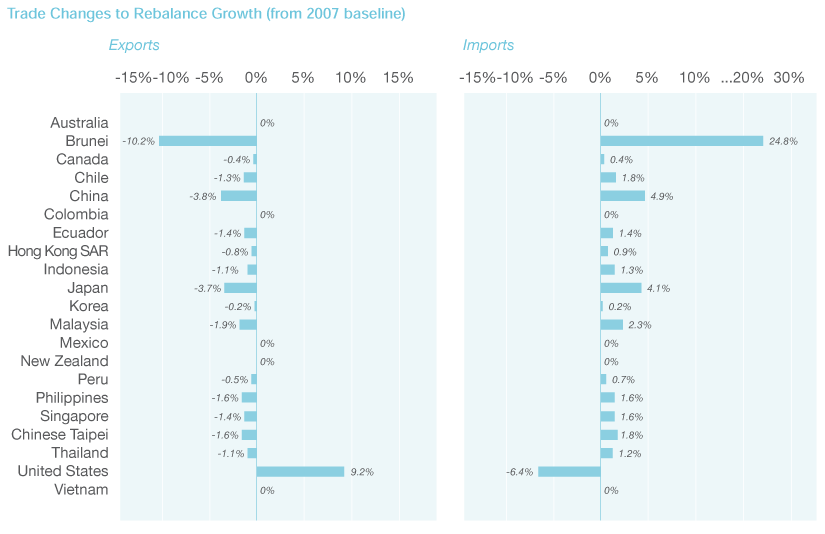

To assess the implications of rebalancing, we used a simple simulation to calculate a pattern of expenditures in 2007 that would have brought U.S. deficits down to sustainable levels. It turns out that this objective could have been achieved with modest expenditure changes. In China, consumption would have had to increase by 4% over the 2007 level – a change normally achieved in 6 months given China’s rapid growth. Somewhat larger percentage increases (5%) would have been required for investment in Southeast Asia and Latin America, and somewhat smaller (2%) reductions in consumption and government expenditures in the United States. Trade changes would have been a little larger: 9% for US exports and -6% for US imports. (The results show large changes for Brunei since that economy's surplus was the region's largest, in relative terms, in 2007. The calculations do not account for special circumstances that might suggest different or smaller adjustments in that case.)

Chart 1-4: Rebalancing Trade

The arithmetic of rebalancing is favorable because imbalances that exert great stress on global financial relations are relatively small compared to broad categories of domestic expenditures in large economies. But the arithmetic tells only part of the story. The politics of these adjustments is likely to be more difficult. Some possible policies are discussed below and in greater detail in the PECC Taskforce report.

Structural policies

Achieving solid, balanced growth will require economies to exit their stimulus programs and to adopt complex and varied structural reforms. These will be difficult to implement technically and politically. For example:

- U.S. policies could impose new disciplines on consumer and government spending by reining in excessive borrowing and by increasing taxes.

- China’s policies could stimulate domestic demand by improving social safety nets, freeing labor markets in order to raise wages, and opening capital markets to smaller firms.

- Japan and other advanced Asian economies could free up service sectors and refocus technological capabilities on growth markets such as aging populations and energy conservation.

- Southeast Asia and South America could accelerate investment through measures that improve productivity and the conditions for doing business.

Sustained growth will also require changes in supply – resource flows to tradable goods industries in the United States and to nontradable sectors, especially services, in Asia. Ultimately, such compositional shifts require significant relative price changes. Exchange rate flexibility (the appreciation of the currencies of China and other Asian exporters vis-à-vis the United States dollar) is the least disruptive way to achieve them, cooperative approaches to this may be useful in bringing about this change.

Within this general framework, each Asia-Pacific economy will face its own challenges – in some, attention will have to focus on household incomes and expenditures, in others investment and infrastructure, and in still others agriculture, resources, or services. The complexity of these changes should not be underestimated, but all are within reach of Asia’s pragmatic, successful approaches to policy. Asia does not need to “throw out the baby with the bathwater;” outward-oriented policies, efficient manufacturing, and high savings remain powerful assets for growth. The challenge in the post-crisis period is to extend market-oriented reforms to more sectors within economies and to more transactions among them.

Growth engines

These demand and supply shifts could be accelerated with high profile Asia-Pacific initiatives. Selected “growth engines” could address important trends – population aging and other social and environmental priorities – and use government expenditures and other incentives to stimulate investment. They could be backed by catalytic commitments from the Asian Development Bank and other international investors. Four important areas for such projects are:

- Economic integration: investments in connectivity and trade agreements that strengthen Asia- Pacific markets.

- Green economy: investments in energy conservation, research and development, efficient irrigation, and energy-saving vehicles and transport systems.

- Social priorities: investments in education, health care, pensions and social safety nets.

- Knowledge and productivity: investments in research and development and technology, and reforms to drive productivity.

Such regional initiatives could stimulate Asian demand, create markets for Asia’s manufactures, engage American resources and technology, and put Asia’s savings to productive use.

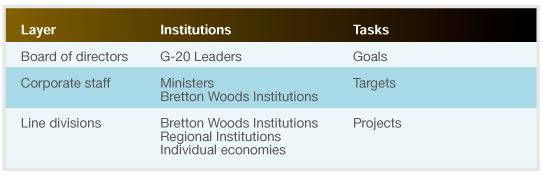

A role for Asia-Pacific institutions

International cooperation will be essential to a successful policy framework. The G-20 now provides a “board of directors” for the global system, with substantial Asia-Pacific membership. But the plans of these “directors” will need to be translated into concrete initiatives and projects. And more inclusive forums will be needed in order to engage economies not in the G-20.

Layered Cooperation

In the Asia-Pacific region, ASEAN+3 could play an important role in orchestrating a smooth realignment of Asian exchange rates relative to the dollar. APEC is also in a good position to help. As a trans-Pacific forum, it spans critical economies and dimensions of rebalancing. It has accumulated expertise on structural reforms and its non-binding format is suited to the complex cooperation required. APEC’s “pathfinder” approach, for example, could provide a platform for initiatives by groups of economies that support specific rebalancing objectives. APEC’s workplan could take on packages to address priority “behind the border” barriers to trade, and engines of growth focused on common social and environmental goals.

Interdependence in the Asia-Pacific region is now often viewed as a source of risk, but it is also a tremendous asset: it connects the most powerful technological, financial, and productive resources ever assembled in history. Asia-Pacific institutions should not miss the opportunity to build on these connections to address the crisis. By working together, Asia-Pacific governments could send a powerful signal to markets that they are committed to cooperation and to holding each other accountable for keeping growth on track.

<< Previous

Next >>